As we enter 2019, it is important to reflect on some of the recent and upcoming changes that will positively impact US regional banks in the coming months and years. Before diving into some of these regulatory changes, we should first define what is considered a “regional bank.” Officially, a regional bank is considered a bank that only operates in certain states that offers the traditional practices of a bank (e.g. retail banking) but does not possess the capital to operate at a national or global level. More specifically, for the sake of this article, we will define a regional bank as one that operates in a specific region of the United States and has under $250 billion in assets. For example, SunTrust Bank (that has recently announced its merger with BB&T) and Fifth Third Bank that operate in the Southeast and Midwest respectively fall within the traditional definition of regional banks (pre-merger for SunTrust).

Introduction & Background

In the aftermath of the 2008 crisis, Congress enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank), a response to the various “bailouts” provided by the Fed under the Troubled Asset Relief Program (TARP). This act affected various aspects of the US financial system including preventing banks from using customer deposits for their own profits, also known as the “Volcker Rule.” Although necessary given the conditions of the US Financial System between 2008-2010, the act served as a major roadblock to banks, especially smaller regional ones, to continue to display strong earnings growth to their investors. Combine this constraint with the advent of Fintech firms providing best-in-class technology and competitive interest rates on loans, and regional banks have found themselves battling serious headwind over the last few years.

In recent years, pressure has mounted on both parties to reform some of the regulations associated with Dodd-Frank, especially those impacting US regional banks, given that the act was originally created in a “one-size fits all” framework without accounting for the size and challenges of some of the smaller players. Considering this, momentum began in 2018 and should carry forward in 2019 and beyond to restructure some of these regulations in a way that facilitates economic growth for non-systemically important financial institutions such as US regional banks.

This article aims at identifying these changes, highlighting some of the impacts associated with them, and ultimately showcasing how Wavestone can assist in ensuring proper adaptation of these reforms.

Recent and Upcoming Regulatory Changes

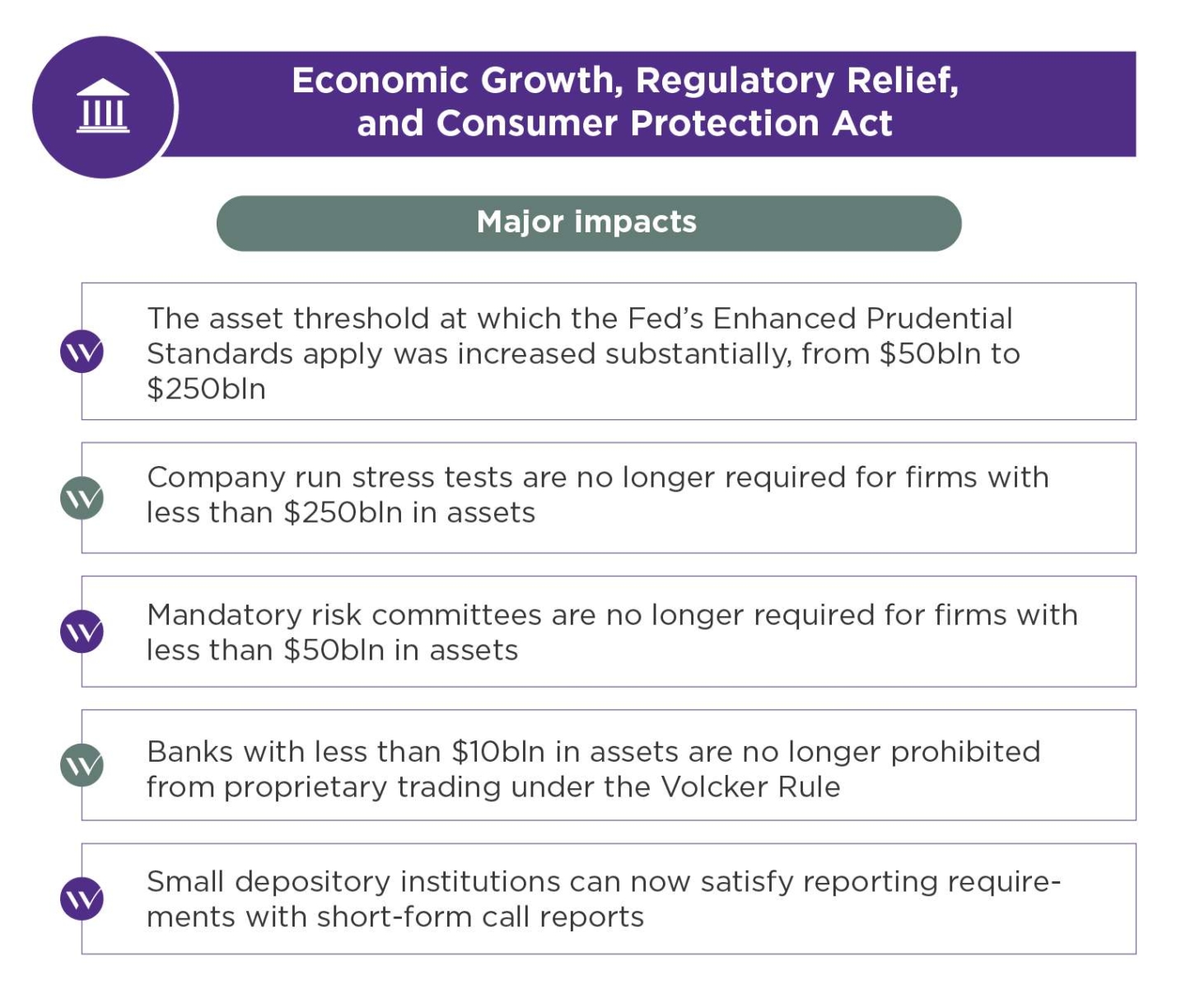

On May 24, 2018, the biggest rollback of bank rules since the Financial Crisis was approved by Congress and signed by the President. This bill, called the “Economic Growth, Regulatory Relief, and Consumer Protection Act,” (EGRRCPA), was largely supported by both parties and served as the first major win for proponents of less stringent banking regulations post-crisis. Though this act was largely applauded by all actors across the financial system spectrum, it was especially celebrated by smaller regional banks, community banks, and credit unions.

Post 2018-Mid-term elections, democratic leadership in the Congress has stated an interest in focusing legislative actions on protecting customers and investors. In November 2018 remarks delivered to the House Financial Services Committee, Representative Maxine Waters, the new Chair of the House Financial Services Committee, confirmed a strong stance of congressional supervision of the American banking system.

Speaking to the same committee, the Federal Reserve’s Vice Chair of supervision, Randal Quarles, aimed focus on the continued loosening of regulations, specifically for community banks with a new community bank leverage ratio proposal. Given the contrasting positions of these critical legislative and financial entities, it is practical to review relevant legislative amendments to be determined in 2019.

Given these changes, what should be the top priorities for US regional banks?

- Optimization of risk and compliance functions: US regional banks must anticipate continued regulatory change and be ready to implement solutions efficiently.

- Stronger investment in Sales & Trading Operations: The rollback of the proprietary trading restrictions on smaller institutions opens an opportunity to invest in human capital and technology to further participate in capital markets activities that regional banks were otherwise previously unable to do.

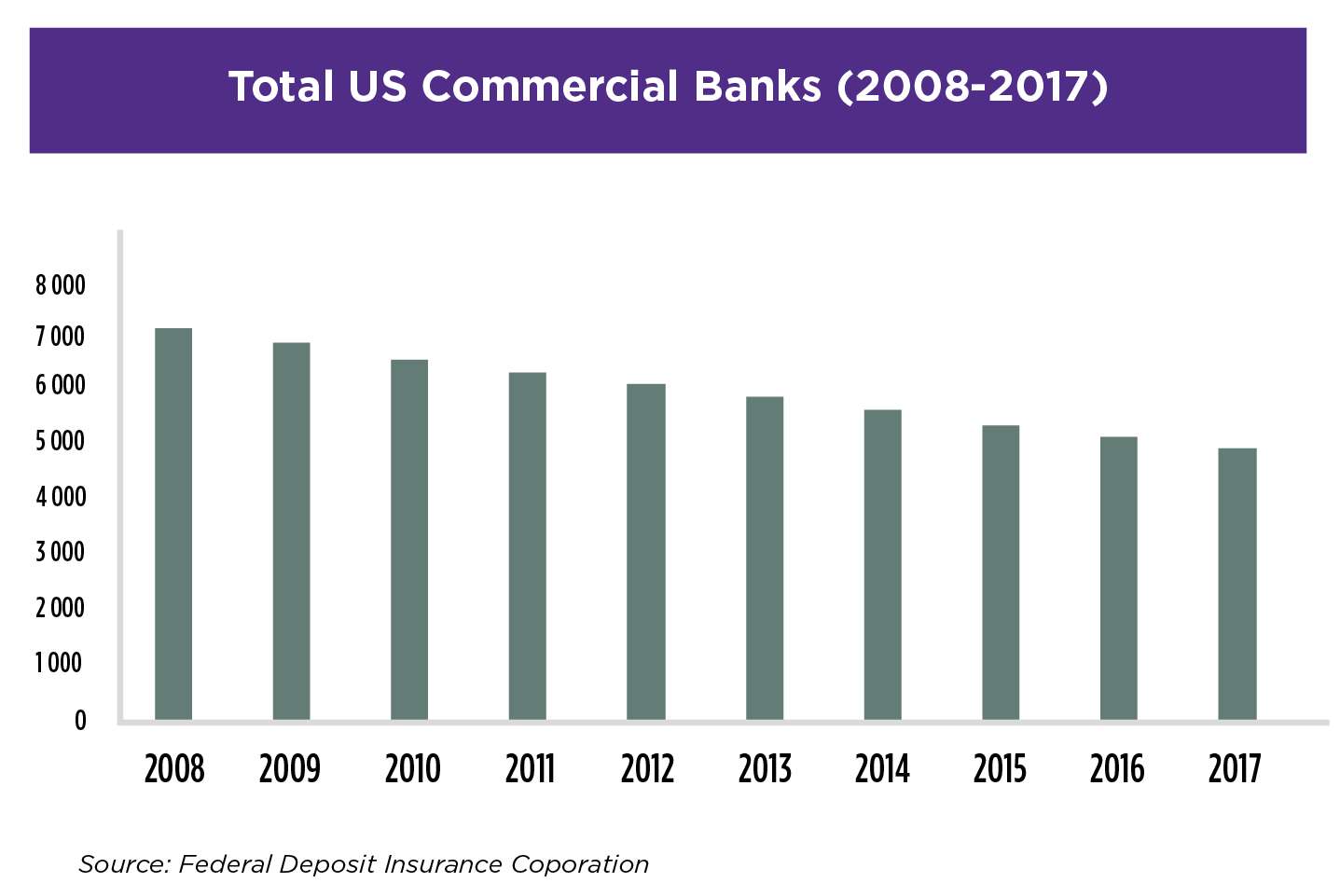

- Awareness of an ongoing trend of US commercial bank mergers and industry consolidation: Over a period of 10 years and several presidential administrations, the number of US commercial banks continues to be on steady decline and mergers play a large role. The inverse relationship between regulations and mergers suggests that this trend of consolidation should be monitored by regional banks (i.e. the easing of regulations generally leads to a less scrutinized antitrust-environment). Additionally, the number of new FDIC-insured bank charters in the US has decreased substantially.

How can Wavestone help?

Our approach to maximizing the benefits of the regulatory relief for US regional banks in 2019 and beyond is centered around our following capabilities:

- Operating Model Design:

- Design optimal operating models to align with the bank’s strategy

- Align governance and organization with new ways of working

- Growth Development:

- Design and review business models to facilitate synergies / cross-selling

- Perform market analysis to quantify and assess business opportunities

- Performance & Process Management:

- Enhance process efficiency through an end-to-end review of existing processes leveraging automation capabilities

- Drive performance management with adapted indicators from a tasks/activities perspective to a more broad financial & budget view

- Post-Merger Integration:

- Create a robust integration planning roadmap to account for the specificities of two distinct organizations

- Manage change from a people, process, and technology perspective

Related Insights