Artificial intelligence (AI) is changing the landscape of markets and causing a technological revolution in how business is being done. A recent report by the World Economic Forum on the projected impact of AI in banking, warns of a changing competitive landscape as small and mid-size banks struggle to adapt to artificial intelligence. As large banks have the money and resources to invest in AI competencies, smaller banks often lack in AI maturity or the investment necessary to reach it. We explore how small and mid-sized banks can overcome challenges and improve AI adoption through two main areas:

- Data Quantity and Quality

- Cost of AI Infrastructure

Data Quantity and Quality

Quantity: Small banks must overcome insufficient data quantity for accurate and effective AI programs

Historically, dominant institutions in banking were built on economies of scale in assets.6 However, the future of artificial intelligence (AI) driving operational efficiencies is increasing the importance of data at scale in presenting cost advantages.6 While banking giants such as Citibank are increasingly using machine learning (ML) and big data to adopt anti-money laundering systems, chat bots, and other AI based programs, small and mid-sized banks struggle with the amount of data needed to deploy similar programs.5 AI tools benefit from scale in data – as quantity increases, so does the ability to recognize patterns and develop insights. Nevertheless, the World Economic Forum concludes that collaborative AI-driven tools, built on shared datasets, can enable more efficient and safer banking for even smaller players. The World Economic Forum also warns that firms will need to be agile and enter into important data sharing partnerships. This stems from a concern that large banks will capitalize on a shift in consumer behavior and eliminate small to mid-sized banks through use of AI. If small and mid-sized banks move to create common utilities and frameworks for their data, AI can be used to develop insights on customer behavior, industry threats, and more.

A few practical examples of data sharing and joint ventures have already emerged in banking:

Nordic KYC (Know Your Customer) Utility

Nordic KYC Utility – 5 banks in the Nordics established a joint anti-money laundering artificial intelligence infrastructure. The infrastructure will also ensure compliance with regulations and requirements related to Know Your Customer (KYC)1.

Royal Bank of Scotland and Vocalink (UK)

The Royal Bank of Scotland and Vocalink coordinated a joint venture to create machine learning and AI system to identify and prevent fraud in small and large business customers².

In small and mid-sized banks there is often an issue in the availability of suitable data. Furthermore, the speed at which AI solutions have entered the market is out-pacing firms’ ability to suitably organize internal data for use. Data is often held in separate silos across departments, on different systems, with internal political and regulatory issues restricting sharing of data, and not recorded as data but informal knowledge of the firm.1 While large banks deal with these same challenges, many have had the money to invest in digital transformation projects that work to mitigate them. Small banks will need to invest in the accessibility and recording of their data to increase overall availability.1 This will in turn increase the ability of banks to coordinate data-sharing AI initiatives.

Quality: With many legacy systems still in place, small banks must undergo digital transformation to improve data quality in order to build AI programs3

Data quality is the most important aspect of AI as the predictive capabilities of models are defined by the breadth, depth, and quality of input data.6 Most financial institutions face similar data challenges in sourcing quality data. However, larger banks are currently putting together the resources to adapt legacy data systems for digitization, and the data to fill AI and ML algorithms.

Overall, the number of actors specializing in improving data quality has risen in recent years. Therefore, both large and small companies have been given the capability to update their legacy systems to prepare for AI programs.5,9 For example, FinTechs like SuperbAI are actually using their AI program for automated data cleaning and collection. By integrating their AI with human-intelligence they drastically decrease the workload of data cleaning.7

Not surprisingly, a global survey of financial service providers, completed by the Digital Banking Report, found that the second most mentioned challenge for AI deployment was the structure of data available.4

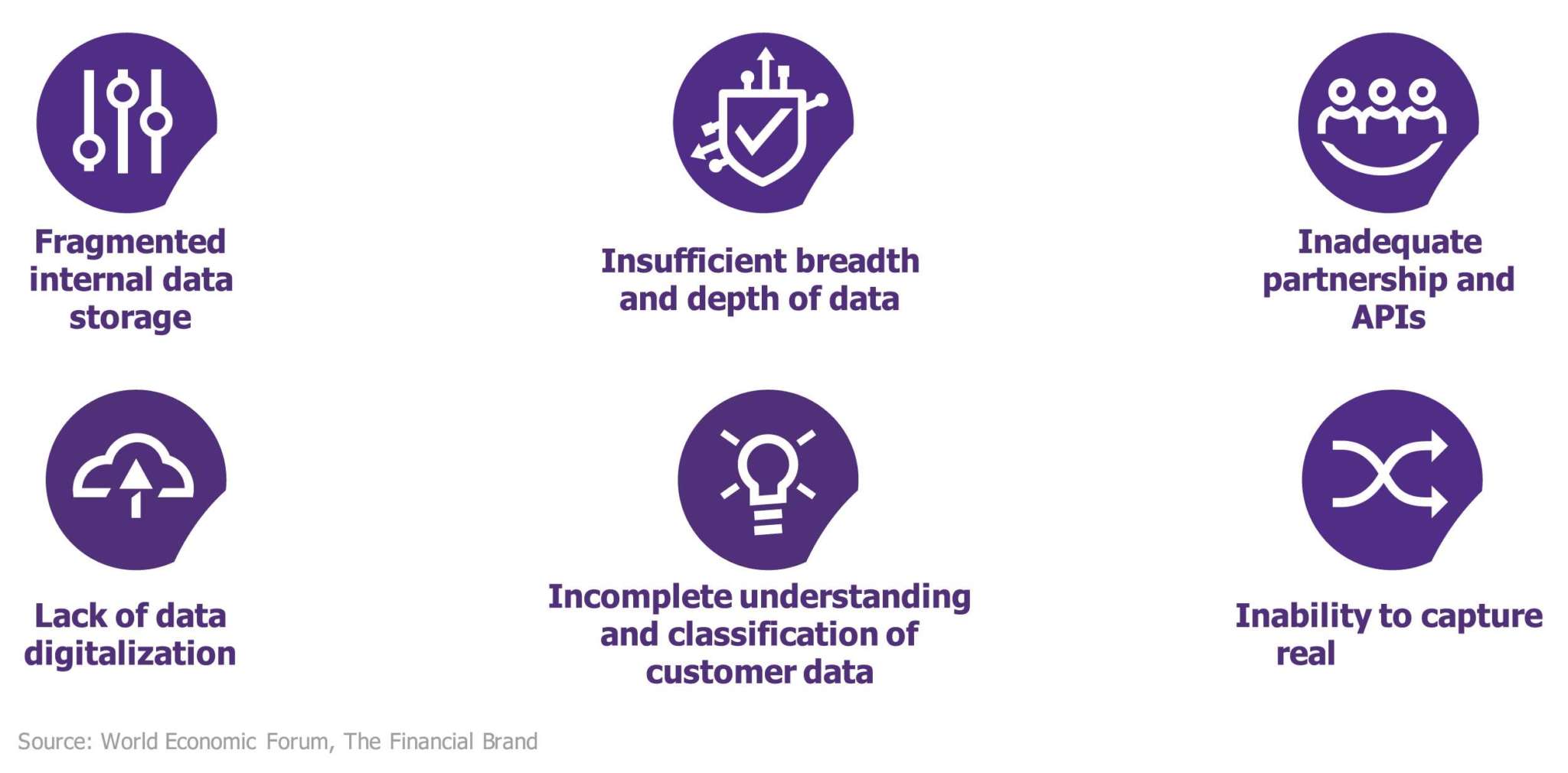

Overall, the main concerns for legacy data systems (especially in small banks) to achieve AI mature data quality include:

Moving forward, small and mid-sized banks need to invest in the quality of their data to lay the groundwork for artificial intelligence programs and the data transformation necessary to survive in a changing industry.

Cost of AI Infrastructure

Cost: Costs associated with AI programs such as data transformation, AI experts, implementation management, have presented a financial challenge for small and mid-sized banks

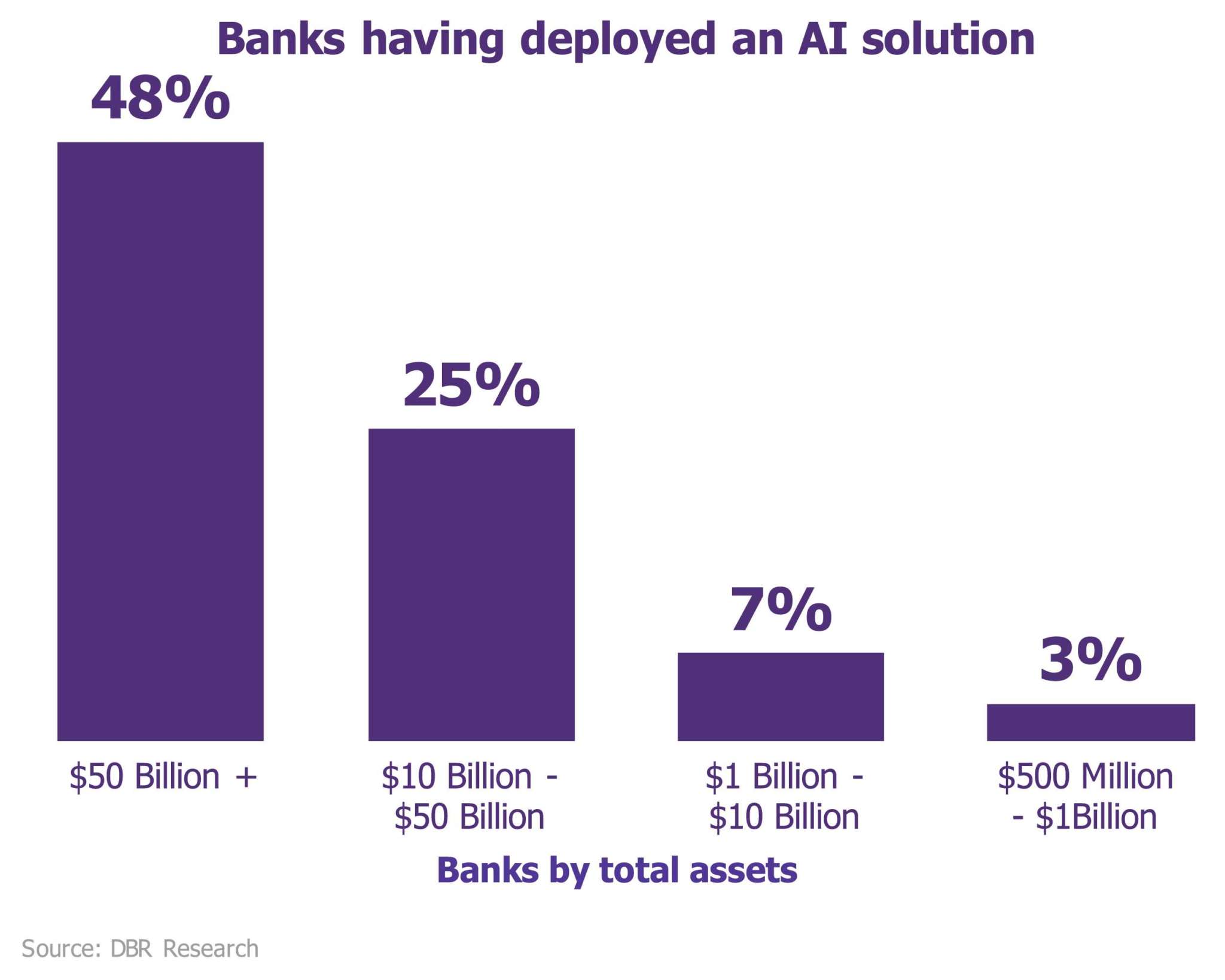

The Digital Banking Report found that firms with fewer assets are lagging in AI and Digital Transformation.

Cited as the largest cost hurdle for smaller banks in adopting AI, is a lack of talent within the company to create or even manage the implementation of AI programs [Digital Banking Report]. As investing in artificial intelligence, and the data quality required, can be extremely costly, most small to mid-sized banks simply don’t have the resources. Large banks’ ability to either hire in-house AI and ML experts, or more likely pay for project work, is a clear advantage.

Nevertheless, there are solutions for small banks to overcome these challenges. For example, data sharing joint ventures (mentioned above) split the cost of hiring experts and engineers. Third-party solutions can also help: for instance, Fusemachines is a startup that looks to “invest in AI talent around the world and integrate them with your organization to build AI solutions.” Their mission to “democratize AI” is exactly what these banks need.8 Lastly, companies with in-house data scientists can help improve the quality and quantity of company data while facilitating efficient implementation of new systems.

Make Investment in AI Worth It

Artificial intelligence is an enormous undertaking that needs to be highlighted

It is important to understand that returns on investment in AI will be realized in the long term and banks must position themselves well to make the investment pay off. A major pitfall of digital transformation and AI undertakings are a lack of visibility to the end consumer.

As returns from these programs take time, small and mid-sized banks need to focus on showing their customers, and the rest of the industry, that they are agile in a rapidly changing marketplace. A study released by Kony, of 800 executives and 800 consumers across four industries, shows that consumers often don’t give businesses credit for the level of investment they are making simply due to lack of awareness.10,11 As corporate and retail customers are increasing demand for digital transformation and its outcomes, communication can be just as important as the AI maturity that banks are striving for. Small and mid-sized banks need to carefully manage this digital undertaking to reach the full potential of these programs and keep up with the rest of the industry.

While the cost of digital transformation and AI programs may be high, there are ways to offset these issues. Moving forward small and mid-sized banks must prioritize improving their data, familiarize the company with initial AI infrastructures, and begin data sharing partnerships or collaboration. If this is realized, they should be able to tap AI and stay on pace with larger banks in the industry.6

Citations

- Aziz, Saqib and Dowling, Michael M., AI and Machine Learning for Risk Management (July 14, 2018). Published as: Aziz, S. and M. Dowling (2019). “Machine Learning and AI for Risk Management”, in T. Lynn, G. Mooney, P. Rosati, and M. Cummins (eds.), Disrupting Finance: FinTech and Strategy in the 21st Century, Palgrave, pp 33-50.. Available at SSRN: https://ssrn.com/abstract=3201337 or http://dx.doi.org/10.2139/ssrn.3201337

- Demetis, Dionysios S. “Fighting money laundering with technology: A case study of Bank X in the UK.” Decision Support Systems 105 (2018): 96-107

- Marous, J. (2017, September 15). Artificial Intelligence Needs a Strong Data Foundation. Retrieved from https://thefinancialbrand.com/67039/ai-hierarchy-of-data-needs/?internal-link

- Marous, J. (2017, November 21). Competitive Survival in Banking Hinges on Artificial Intelligence. Retrieved from https://thefinancialbrand.com/67890/

- Maskey, S. (2018, December 05). How Artificial Intelligence Is Helping Financial Institutions. Retrieved from https://www.forbes.com/sites/forbestechcouncil/2018/12/05/how-artificial-intelligence-is-helping-financial-institutions/#63849352460a

- World Economic Forum. (2018). The New Physics of Financial Services – How artificial intelligence is transforming the financial ecosystem. Retrieved from https://www.weforum.org/reports/the-new-physics-of-financial-services-how-artificial-intelligence-is-transforming-the-financial-ecosystem

- (2019). Data Collection. Retrieved from: https://www.superb-ai.com/data-collection

- (n.d.). Company Overview. Retrieved from https://www.fusemachines.com/company-overview/

- Groenfeldt, T. (2019, January 11). Smaller Financial Firms Struggle To Match Big Bank Digital/Mobile Innovation. Retrieved from https://www.forbes.com/sites/tomgroenfeldt/2019/01/11/smaller-financial-firms-struggle-to-match-big-bank-digitalmobile-innovation/#7ee0b64d28e5

- Kony Digital Experience 2019 Index Survey. Retrieved from http://forms.kony.com/rs/241-GBN-089/images/Kony_Digital_Experience_Survey_09.pdf

- McKendrick, J. (2019, July 25). Trillions spent on digital transformation and customers don’t notice. Retrieved from https://www.zdnet.com/article/the-trillions-spent-on-digital-transformation-seem-invisible-to-customers/?mkt_tok=eyJpIjoiWWpCak5tWTJOekJrTVdSaSIsInQiOiJ4bkR4YVUyWHhJREZrcm5ueGNcL0drR01GV09qTzN6eHBCbFBLZ25aaG5pQkliOWlUb2NsUmt1V3p0WXRrRFIrbTR2RUxEcFIwTm1cL1htMENCXC9hdm9GTHdMck94WWU4UGY1QnRnSUxFa0xPenNqUHJWRFQ4TkdKcE03djdyRnJ0MSJ9

Related Insights